![[Day2]Panoramic VR takes you to the “cloud” of the World Manufacturing Conference](https://img.chinait.com/chinait-en/2021/11/193033.jpg)

Text|Huang Xin

(ChinaIT.com News) The semiconductor industry and its supply chain play a key and fundamental role in the development of emerging technologies, no matter in terms of trade scale or future-oriented development and application fields, which can be compared to oil and natural gas as strategic resources.

In view of its special and increasingly important status, its role in international relations and geopolitics has become increasingly prominent, and it has attracted great attention from the governments and business leaders of major producing countries. Some countries even use foreign policy tools to expand and optimize their domestic industrial investment scale and investment environment, and consolidate their industrial advantages.

In 2022, global semiconductor sales will exceed 500 billion US dollars, which is an irreplaceable promoter of global economic activities.

According to Accenture’s estimates, traditional IC chip production must span more than 70 countries(area)to deliver the final product to the consumer. Leading chip sellers typically have tens of thousands of suppliers scattered around the world. Understanding the structure of the global semiconductor manufacturing landscape is critical for policymakers as they aim to navigate changing, globally-spanning supply chains.

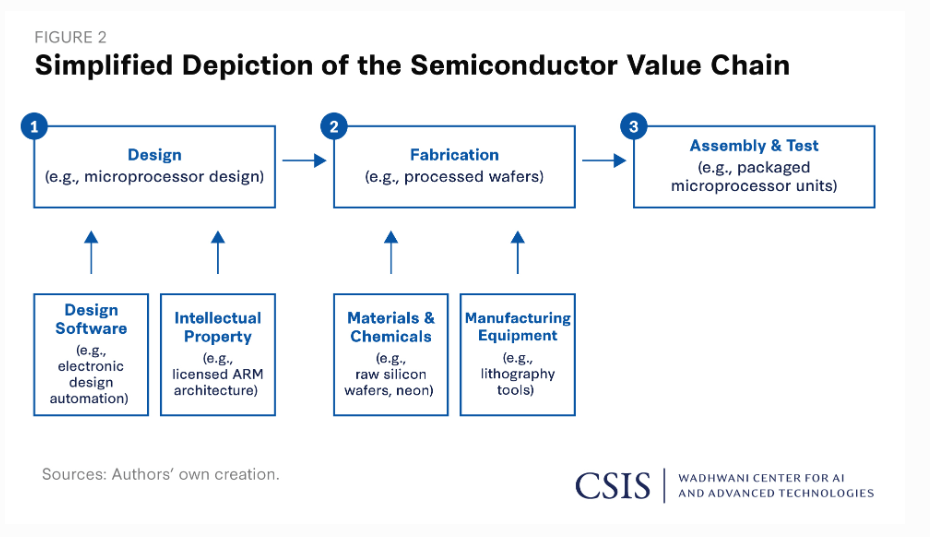

(1) Design

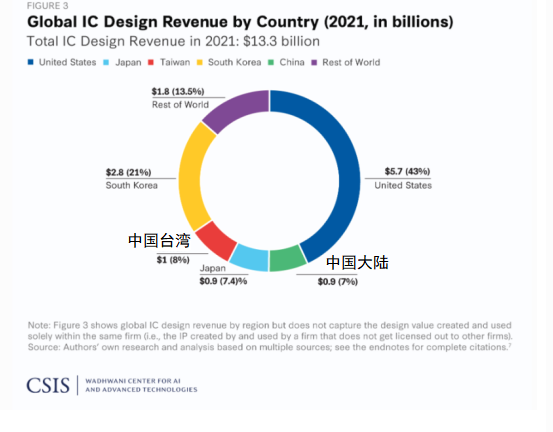

The United States is in a leading position in the field of semiconductor design, and American companies occupy more than 40% of the global IC design market share, including EDA, semiconductor IP and design services.According to Georgetown University’s Center for Security and Emerging Technologies(CSET)According to the data, US companies controlled more than 50% of the core IP market share in 2019.

The total global EDA market revenue in 2021 will be USD 8.27 billion. The US is also leading in EDA. In 2021, three US companies – Cadence, Synopsys and Mentor Graphics(U.S. subsidiary of Siemens, Germany)Occupied 70% of the EDA market.

Chip design software is highly centralized and plays a vital role in the value chain. The latest advanced chips cannot be designed without the latest software. In 2021, the U.S. Department of Commerce will impose export controls on certain types of EDA software, restricting Chinese companies’ access to U.S. EDA technology.

Similar to EDA software, the United States is also in a leading position in the production and licensing of core IP. US and UK companies such as Intel, Cadence, and ARM are leaders in semiconductor IP. According to CSET estimates, the United States and the United Kingdom together accounted for more than 90% of the global core IP market in 2019.

(2) Manufacturing

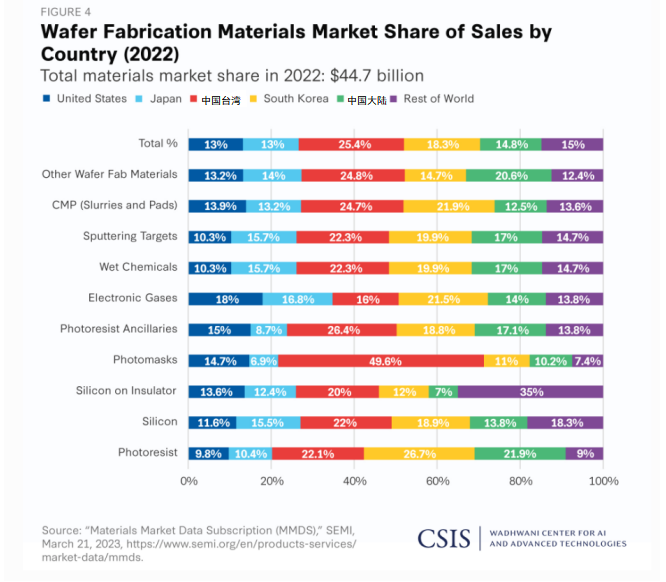

1. Semiconductor materials and chemicals

Raw and man-made materials, such as silicon wafers, photomasks and photoresists, as well as chemicals for semiconductor materials, are necessary inputs in the semiconductor manufacturing process. In 2021, the global semiconductor materials market will exceed US$40 billion, concentrated in the United States, Germany, Japan, Taiwan, South Korea, and mainland China. In 2021, Taiwan, China will account for 25% of the global materials market share in terms of sales.Europe(9%)and mainland China(15%)relatively small market share. Although Europe’s total sales are modest, it holds a key position in the materials supply chain, especially in the supply of chemicals. Mainland China mainly supplies primary products such as gallium, tungsten and magnesium needed to make semiconductors.

Silicon wafers account for the largest share of the materials market, accounting for 1/3 of total sales of semiconductor materials in 2021. Over the past 20 years, the market concentration of silicon wafer suppliers has continued to increase. The number of companies providing critical supplies has shrunk from more than 20 in 1990 to five in 2020. These five companies control approximately 95% of the global silicon wafer market. Diameter 300mm(approximately 12 inches)Silicon wafers, which represent cutting-edge chips, are supplied by companies based in Japan, Taiwan, Germany and South Korea. Japan’s Shin-Etsu is the world’s largest silicon wafer maker, accounting for 29.4% of the global market share in 2020. Sumco(Japan)、Global Wafers(U.S)Shichuang Electronic Materials(Germany)SK Shichuang Electronic Materials(South Korea)and Soitec(France)Together, they account for 65% of the global silicon wafer market. Mainland China has relatively limited capacity to produce 300mm/12-inch silicon wafers, delaying its development in the material supply chain.

The supply of photomasks and photoresists is mainly dominated by Japanese, Taiwanese and Korean companies. The photomask market will reach $5.5 billion in 2021, and the photoresist market will reach $2.7 billion. China cannot produce state-of-the-art photomasks and has limited capacity to produce advanced photoresists.

2. Manufacturing equipment

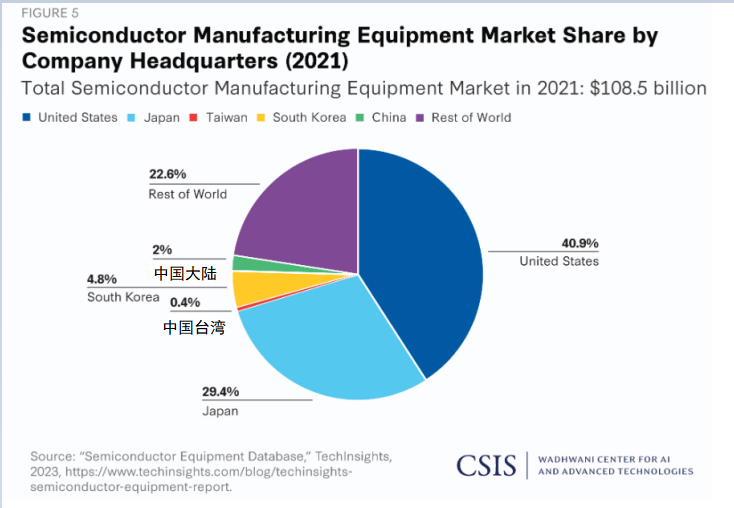

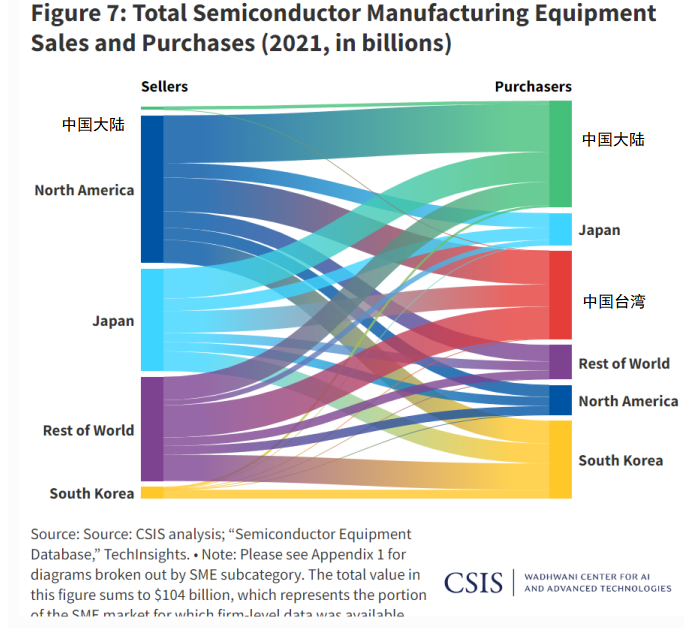

Most of the world’s fabs are located in the Indo-Pacific region and the United States, and equipment suppliers headquartered in the Indo-Pacific region account for the global semiconductor manufacturing equipment(SMEs)77% of market sales.In addition, companies in the Indo-Pacific region are also the largest purchasers of SMEs – in 2021, the region purchased more than $104 billion worth of wafer fabrication, packaging and test equipment(excluding advanced packaging equipment).

The United States and Japan have the largest share in the SME industry. American companies alone account for more than 40% of the global SME market, followed by Japanese companies, accounting for 29%. Along with the Netherlands, firms from these three countries dominate the supply of SMEs. There are no strong SME suppliers in Taiwan and China.Major semiconductor manufacturing countries in the Indo-Pacific region(area)Among them, China Taiwan is the region with the smallest SME industry scale, and the SME produced in mainland China accounts for less than 2% of the global supply. Although the scale of production in South Korea is small, its technology is relatively mature, accounting for 4.8% of global sales in the SME industry.

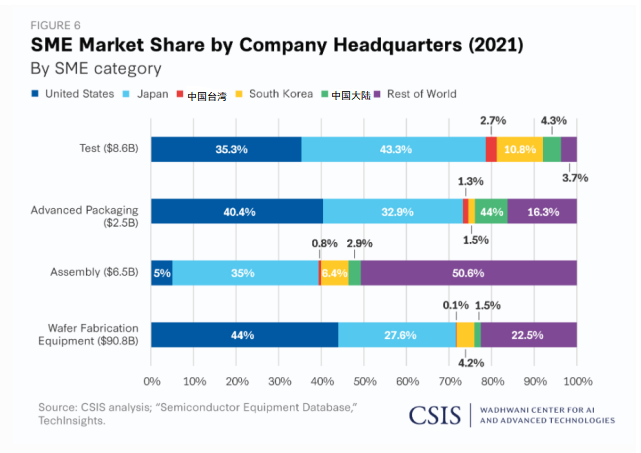

Among SMEs, the U.S. leads in fabs and advanced packaging equipment, and Japan leads in packaging and testing equipment. The United States and Japan supply more than 70% of fab equipment for global semiconductor production. South Korea plays an important role although it only accounts for 4.2% of the global market share.

In terms of packaging equipment, Japan’s strength is second only to Europe. Japan leads the way in test equipment, accounting for about 43% of the global market share. The United States and South Korea accounted for 35.3% and 10.8% respectively.

The United States and Japan are the main producers of SMEs in the Indo-Pacific region, providing equipment for other companies in the Indo-Pacific region; 90% of SMEs produced in the United States and Japan are sold to the Indo-Pacific region. Equipment makers in mainland China and South Korea generally serve their respective domestic markets, although they also supply a small amount of equipment. Although the sales volume is very small, 98% of the SMEs produced in mainland China are sold to local companies.Korean SME manufacturers sold about 73% of their production to Korean companies(Manufacturing facilities of some of these companies are located outside Korea). Leading Korean SME manufacturers include SEMES, Wonik IPS, PSK and Eugene Tech.

China has been the largest SME market in the Indo-Pacific region in recent years, procuring more than $28 billion in equipment in 2021. It is worth noting that 30%, 29% and 20% of SME sales in the United States, Japan and South Korea were sold to customers in China. China buys 45% of its total SME volume from the US and 28% of its total SME volume from Japan. It is expected that in 2023, South Korea will overtake China and become the largest purchaser of SMEs.

(1) Wafer manufacturing equipment

Manufacturing Equipment by Wafer(WFE)Calculated by sales, the United States accounts for 44% of the global market share. Mainland China was the largest buyer of US WFE, followed by South Korea and Taiwan. More than half of the WFE in mainland Chinese fabs comes from the United States, most of which come from three companies: Applied Materials, LAM Research and KLA Tencent. The vast majority of U.S. WFE sales in China consist of deposition and related tools, etch and cleaning tools, and process diagnostic equipment. Over the past five years, U.S. WFE suppliers have nearly tripled their revenue from the Chinese market, from $3.7 billion in 2017 to $12.4 billion in 2021.

After China, South Korea and Taiwan are the second largest importers of WFE in the Indo-Pacific region(area), the purchases in 2021 will exceed 20 billion US dollars, of which 42% and 40% will come from the United States. Although Japan’s procurement volume is relatively limited, and the procurement scale in 2021 is only 7.9 billion US dollars, it also relies on the United States, with 48% of its purchases from the United States.

Japan is a major producer of lithography and masking equipment, etching and cleaning tools, and deposition and related tools.Dutch ASML is the latest generation of lithography scanning equipment(Deep ultraviolet DUV or extreme ultraviolet EUV lithography machine)The sole supplier of EUV, but Japan’s Nikon and Canon can provide non-EUV lithography machines and scanning equipment. Japan is the second largest supplier of lithography and mask equipment to mainland China, after the Netherlands. Lithography equipment in mainland China mainly comes from ASML and Japanese companies, and purchases more than tripled from 2017 to 2021.

Japanese WFE manufacturer in Korea($4.6 billion in sales in 2021)and Taiwan($4.5 billion in sales in 2021)Also has a lot of business, and relatively little in the non-Indo-Pacific region(total sales of less than $2 billion in 2021).

(2) Assembly, testing and packaging equipment

Semiconductor Manufacturing Backend – Assembly, Test and Packaging (ATP)— is typically less capital intensive than wafer fabrication. The size of the ATP equipment market is relatively small, totaling $15.2 billion in 2021, compared to $90.8 billion for WFE.

Japan is the largest supplier of packaging equipment in the Indo-Pacific region, with an export volume of more than US$2 billion in 2021. The packaging equipment produced in Japan has a market share of 66% in the country, 40% in Taiwan, 24% in the United States, 29% in mainland China, and 29% in South Korea. Major producers in Japan include DISCO Corporation, TOWA Corporation, and Accretech (Tokyo Seimitsu).

Japan’s position in the test equipment market is also critical. China and Taiwan host most of the world’s ATP factories, most of which are equipped with Japanese equipment from Advantest, Tokyo Electron and Accretech. Test equipment produced in Japan accounts for 47% of the Taiwan market, 53% in mainland China, and 35% in South Korea.

The United States has a 35 percent share of the global test equipment market, trailing Japan. South Korea came in third with an 11% share.

3. Wafer fabrication plants

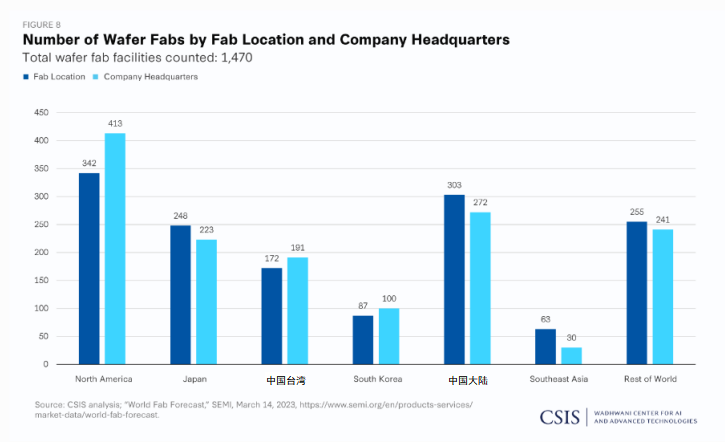

Indo-Pacific region(including US)Owns most of the semiconductor wafer fabrication plants in the world.Of the 1,470 confirmed fabs globally, 1,215 are located in the Indo-Pacific region and 1,229 are operated by companies headquartered in the Indo-Pacific region(including US).

The announced fabs are mainly concentrated in the United States, mainland China and Taiwan, with 24, 19 and 17 new fabs planned to start construction before December 2024, respectively.

However, only a few fabs have the capabilities and infrastructure required to manufacture advanced-node semiconductors.For artificial intelligence, quantum and high-performance computing, and other critical and compute-intensive technologies(compute-heavy technologies)advanced applications, advanced node chips(16nm or smaller)is essential. According to data from the US Semiconductor Industry Association SEMI, US companies own or operate the largest number of fabs capable of producing advanced wafers, reaching 61. These companies are capable of processing silicon wafers 12 inches or larger. China Taiwan followed closely with 44 companies.

As of January 2022, U.S. companies operate 11 fabs in mainland China, one of which is capable of producing 12-inch wafers.South Korean companies, mainly Samsung and SK Hynix, also operate 11 fabs in China, most(7 companies)Wafers up to 12 inches in diameter can be produced. China Taiwan has 13 fabs in the mainland, 8 of which can process wafers below 6 inches, and 2 are capable of processing wafers below 8 inches.

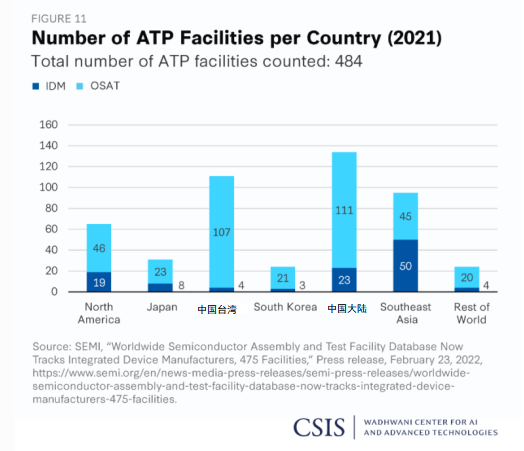

(3) Assembly, testing and packaging

Today, the vast majority(above 95)of ATP plants are deployed in the Indo-Pacific region, and a large number of OSAT suppliers are concentrated in Taiwan, China and Southeast Asia(especially Singapore, Malaysia, Vietnam and the Philippines)area.Among the 484 factories counted by SEMI(2021)134 are located in mainland China, accounting for 28% of the total.

(1) Major countries attach great importance to semiconductor industry policies

Major countries have launched national-level development initiatives, emphasizing the strengthening of semiconductor supply chains to achieve national security and geopolitical goals.

-

In August 2022, the United States passed the “Chip and Science Act” and allocated nearly 50 billion U.S. dollars to improve the United States’ semiconductor manufacturing capabilities.

-

In May 2022, the Japanese government passed legislation to promote “economic security,” which includes a series of initiatives: protecting supply chains for key products, including semiconductors; protecting infrastructure; supporting innovation and technological development through research and development; and creating a confidential patent system.

-

In March 2023, South Korea’s new round of chip stimulus plans made progress. The National Assembly of South Korea holds a plenary session in Seoul and passes the K-Chip Act(K-Chips Act)aims to stimulate investment by giving corporate tax incentives to boost South Korea’s local chip industry.

-

In April 2023, the “European Chip Act” won the tripartite consensus reached by the European Parliament, the European Council and the European Commission, and will invest 43 billion euros in the semiconductor industry. The goal is to increase the share of chips made in Europe to 20% of the world by 2030.

-

In May 2023, the UK pledged to spend £1 billion over the next decade($1.24 billion)to bolster its domestic semiconductor industry and fund a long-anticipated strategy to engage in the battle for global chip market dominance.

Regarding the future of the global semiconductor industry, the CSIS report believes that these policies will evolve into future market competition. Substantial government subsidies are involved in current and proposed future policies. These subsidies are beyond the capacity of the current government, but if given the “new mission” of national security and technological sovereignty, it will accelerate the transformation of the global semiconductor industry. These changes will be more dramatic in the Indo-Pacific region, and policymakers should assess the status and role of the Indo-Pacific region in the global semiconductor supply chain.

(2) The United States will win over more allies to rebuild the semiconductor supply chain

Globally, and especially in the United States, trade, economic, and technology competition policies are undergoing dramatic changes. Issues traditionally in the realm of national security have increasingly permeated national economic policy.Parallel to this shift, the United States is moving away from traditional free trade agreements centered on market access and tariff liberalization(FTA), turning to policies that target sustainable development and labor without providing additional market access. The two moves have been part of a new U.S. industrial policy aimed at strengthening U.S. high-tech competitiveness while preventing foreign adversaries from acquiring advanced technology.

Biden administration is passing Indo-Pacific economic framework(IPEF)and other new multilateral mechanisms to complement its new domestic industrial policy. IPEF has 14 members, including the United States, and covers issues such as trade, supply chains, decarbonization and infrastructure, as well as anti-corruption and transparency. Among them, the supply chain pillar includes specific content for identifying key areas and commodities. The multilateral framework aims to increase the resilience and scale of investment in these key areas, enhance relevant information sharing and transparency, improve supply chain logistics, and protect labor.

Countries in the Indo-Pacific region vary widely in terms of semiconductor production capabilities. Countries such as Japan and South Korea have advanced semiconductor manufacturing capabilities and have established institutional systems to facilitate domestic business development. Other countries, such as Thailand and India, are keen to accelerate the development of their domestic semiconductor industries. Australia, New Zealand, and the Philippines, with little semiconductor capacity, are in some cases unwilling to make the investments necessary to localize a competitive microelectronics industry.

1. Japan

Japan is a leader in machine tools, materials and semiconductor equipment and an ally of the United States. In the 1980s, Japan accounted for 50% of global semiconductor production. Today, Japan accounts for 6 percent of the world’s logic, micro, memory, and analog chips, partly because of U.S. trade policy toward Japan and the country’s failure to move from traditional semiconductor vertical integration to horizontal division of labor.Nevertheless, Japan with its semiconductor storage products(especially NAND),semiconductor(CMOS)International competitiveness in image sensors, advanced immersion lithography and power semiconductors, remains one of the world’s semiconductor industry leaders. Japan’s main advantage in this industry is its huge influence on semiconductor manufacturing equipment and materials, accounting for 35% of the global semiconductor manufacturing equipment supply and 50% of the global semiconductor material supply.

In May 2022, the Japanese government passed legislation to promote “economic security,” which includes a series of initiatives: protecting the supply chain of key products, including semiconductors; protecting infrastructure; supporting innovation and technological development through research and development; and creating a confidential patent system, among others. In July 2022, the United States and Japan established a semiconductor high-level dialogue mechanism and a joint research center to focus on next-generation semiconductors.

Japan recently launched a bilateral public-private partnership on semiconductors, the development of which aims to achieve mass production of 2nm chips. Japan’s Ministry of Economy, Trade and Industry provided about $550 million in investment, with private sector investments totaling $2.4 billion. In the future, these projects will need to inject a lot of money, otherwise they will not be able to successfully change the global supply chain.

2. South Korea

South Korea is a global leader in memory chips and a plurilateral player eager to expand in the U.S. market. As of 2020, South Korea’s global semiconductor market share is 18.4%, accounting for 56.9% of the global memory chip market. In 2020, South Korea’s total semiconductor exports will be US$99.2 billion, of which memory chips will be US$63.9 billion, accounting for 64.4%. Semiconductors are South Korea’s main export, accounting for 19.3 percent of South Korea’s total exports as of 2020.

South Korea sees a strong semiconductor industry as its mainstay. In response to the shortage of semiconductors caused by the COVID-19 pandemic, the Special Law on Enhancing and Protecting the Competitiveness of National High-Tech Strategic Industries specifies that “national high-tech projects” including semiconductors receive tax incentives, regulatory incentives, and other preferential treatment to stimulate R&D and increase production. The National Assembly of South Korea also passed the National Advanced Strategic Industries Act during the administration of President Moon Jae-in, authorizing the Minister of Trade, Industry and Energy to supervise the export of advanced semiconductors to foreign companies. Current President Yoon Seok-yue has also announced his intention to make South Korea a “semiconductor superpower” and will train more semiconductor professionals by expanding the number of admissions for university engineering majors.

South Korea is a member of the Chip 4 Alliance along with the United States, Japan and Taiwan. However, concerns about competition between Taiwanese, South Korean, Japanese, and U.S. firms may limit coordination across markets. Given South Korea’s strong semiconductor industry and China being its largest semiconductor trading partner, it is unclear whether the country will fully support the U.S. export control policy against China. South Korean semiconductor manufacturers have been granted a one-year exemption from export controls on October 7, 2022, and the uncertainty brought about by export controls has made Korean companies face a dilemma. In the future, the United States may encourage South Korea to join the trilateral arrangement between the United States, Japan and the Netherlands, but the extent to which South Korea will accept it is still uncertain. As of May 2023, South Korean companies have obtained a one-year waiver extension from the US, buying time to maintain their business in China.

In addition to regulations, the United States is actively attracting South Korean companies to invest in the United States, and Samsung is a major player in the Korean semiconductor industry. The company is considering building 11 new semiconductor factories in the United States over the next 20 years.

3. Malaysia

Semiconductors are playing an increasingly important role in the Malaysian economy, especially in the field of advanced packaging. The Malaysian legal framework provides strong intellectual property protection for the semiconductor industry and provides attractive conditions for multinational companies to do business in the country. Relatively cheap labor and local talent have made Malaysia a manufacturing hub for electronics since the 1970s.The Malaysian semiconductor industry is mainly composed of assembly, testing and packaging(ATP)and outsourced semiconductor packaging and testing(OSAT)composition. Malaysia accounts for approximately 4% of the global ATP market share.

With a high concentration of facilities established by foreign investors through OSAT, Malaysia has the expertise, equipment and infrastructure needed to increase ATP’s capacity.

In April 2014, the United States and Malaysia upgraded their bilateral relationship to a comprehensive partnership. Malaysia is the 17th largest trading partner of the United States. As of 2020, US direct investment in Malaysia has reached US$13.5 billion. In May 2022, Malaysia and the United States signed a memorandum of cooperation on semiconductor supply chain resilience(MOC). The MOC was signed to emphasize the importance of US-Malaysia cooperation in “creating a resilient, secure and sustainable semiconductor supply chain”; building trust, improving transparency and promoting investment in semiconductor supply chains in both countries.

4. Singapore

Singapore has a strong semiconductor industry, and the country is committed to strengthening its position as a technology and innovation hub.Semiconductor manufacturing accounts for more than 80% of Singapore’s electronics manufacturing output and a share of GDP(GDP)7%. Singapore accounts for 11% of the global semiconductor market. 20% of the world’s semiconductor equipment is manufactured in Singapore. In December 2020, the Singaporean government announced an R&D budget of US$25 billion for the next five years, a 30% increase from the previous five-year budget.

Singapore’s political and economic positioning has attracted a large number of companies seeking to diversify their manufacturing base and supply chain. With its favorable tax and regulatory environment and highly skilled manpower, Singapore is one of the top destinations for investment in high value-added manufacturing. It also has a strong intellectual property protection regime.

The US and Singapore maintain a strong trade relationship, with the US-Singapore Free Trade Agreement signed in 2004. In August 2021, the United States and Singapore also finalized several agreements to expand cyber security cooperation. MEMSIC is committed to building partnerships that foster growth and innovation, and build resilient supply chains.

5. Vietnam

Vietnam is a country in the ascendant, its manufacturing capacity can partially replace China, and it is also the target country of the US “friendly shore outsourcing”. Since the beginning of the 21st century, some global manufacturing companies have entered Vietnam, and large multinational companies have invested heavily to promote the development of Vietnam’s industry. The Vietnamese government offers incentives for high-tech projects, including lower corporate taxes. To develop high-tech enterprises, the Vietnamese government has established a task force to attract technology investment by offering customized incentives to foreign investors. Vietnam has a strong team of engineers, and the cost is relatively low.

Samsung Electronics is Vietnam’s largest foreign direct investor in semiconductors. In 2013, the company invested in the construction of motherboards and electronic components enterprises in Vietnam, with an investment scale of 1.3 billion US dollars. As of 2021, Samsung’s investment has accumulated more than 18 billion US dollars. Samsung has six factories in Vietnam and is building a new research and development center in Hanoi.

The United States is increasingly attaching importance to cooperation with Vietnam. Since the United States and Vietnam concluded a bilateral trade agreement in 2001, the United States has become Vietnam’s largest export market and second largest trading partner.

6. India

India is an active participant in the global semiconductor ecosystem, and while the US-India strategic alliance remains elusive, India remains an important member of the IPEF supply chain pillar. India’s semiconductor demand is around $24 billion and is expected to reach $100 billion by 2025. The country’s semiconductor demand is entirely dependent on imports. In December 2020, the Indian government issued a letter of intent, expressing its intention to establish and expand existing semiconductor wafer fabrication plants in the country, or otherwise acquire semiconductor factories outside India.

In 2013, IBM and STMicroelectronics cooperated with the Indian government to invest 7.91 billion US dollars to establish India’s first chip manufacturing plant. In order to speed up the infrastructure construction of India’s semiconductor and electronics industry, the Indian government proposed to set up an electronic development fund of US$1.58 billion to promote electronic hardware manufacturing in the country.

By 2030, the bilateral trade volume between the US and India will grow to 500-600 billion US dollars. However, the development of bilateral economic and trade relations has not been smooth, and the US believes that India is unwilling to make major concessions. India co-launched the Critical and Emerging Technologies Initiative with the US in May 2022, focusing on a range of issues from innovation ecosystems to advanced defense industry cooperation and building resilient semiconductor supply chains.

On trade policy, however, persistent differences between the US and India have prevented the two sides from reaching a formal bilateral free trade agreement.US decides India no longer eligible for GSP(GSP)standards, and India’s GSP status was revoked in 2019. In addition, after the Russia-Ukraine conflict, the complex military procurement and energy relationship between India and Russia has hindered in-depth cooperation with the United States.

7. Thailand

Thailand’s political uncertainty and relatively high labor costs limit its deeper economic integration with IPEF partner countries. Thailand is the 13th largest electronics exporter, producing everything from semiconductors to storage devices. Thailand’s largest product export category is electronic components and equipment, with an export value of US$42 billion in 2021. The Thai government has stepped up efforts to educate the workforce to support electronics manufacturing and to incentivize foreign investors with competitive tax incentives. In 2021, Thailand announced an initiative to attract semiconductor, packaging and digital industries to Thailand. The Thai government’s foreign investment regulatory framework encourages market entry through tax and non-tax incentives.

However, Thailand lags behind in attracting more foreign high-tech investment, especially compared with neighboring countries such as Vietnam and Malaysia, where its labor cost advantage is significantly weaker than both countries. Political uncertainty in Thailand has investors on their toes. While IPEF presents an opportunity for Thailand to deepen its participation in the semiconductor supply chain, there is a risk of being overtaken by other partner countries.

8. Indonesia

Indonesia’s growing geopolitical influence, large workforce and many key resources could facilitate its development as a semiconductor producer. Java, Sumatra and Kalimantan are rich in silica, and Indonesia has the world’s largest nickel reserves. Even Indonesia has proposed an OPEC-like organization focused on managing nickel exports. The development of nickel mines has given Indonesia an ambition to “create a key player in the electric vehicle industry”. Indonesian President Joko Widodo has said that Indonesia will build new chip design facilities and a new polysilicon plant in Central Java. Under the “Indonesia 4.0” plan of the Ministry of Industry, the electronics manufacturing industry is one of the five key development priorities of the Indonesian government.

The Indonesian government’s prioritization of the semiconductor industry is backed by huge tax incentives. The country’s 19 special economic zones offer additional tax, duty and excise exemptions as well as flexible immigration policies. However, the researchers found that a lack of domestic branded companies or a strong domestic supplier base, combined with a lack of skilled labor, are key obstacles to developing indigenous semiconductor capacity in Indonesia. Additionally, Indonesia’s requirement for local content poses a serious hurdle for potential investors.

The United States and Indonesia cooperate in multiple economic frameworks, such as the Association of Southeast Asian Nations(ASEAN)Regional Forum, East Asia Summit, Asia-Pacific Economic Cooperation(APEC)Forum and G20. However, the country remains on the U.S. priority watch list for 2021. Corruption is another key hurdle for semiconductor companies looking to establish operations in Indonesia.

9. Philippines

The Philippine market is ripe for opportunity. However, it is constrained by ongoing rule of law and corruption issues.The Philippines accounts for the world’s IC(IC)2.8% of exports, ranked among the top 10 exporters in the past decade, performed well in assembly and testing. As of 2022, the Philippines’ trade in semiconductors and electronics is worth $19 billion, accounting for 59.6 percent of total merchandise exports. Exports are mainly driven by the automotive electronics, consumer electronics, and electronic data processing industries, which will see significant growth in 2022.In the 2023-2028 development plan released by the National Economic Development Board in January 2023, the Philippine government prioritized the implementation of the global value chain(GVC)Oriented priority industrial clusters bring opportunities for the growth of industry, manufacturing and transportation.

In 2022, the amendments to the Foreign Investment Law and the Public Service Law have changed the investment environment in the Philippines, and foreign capital has more room for development in the Philippines.

The United States is one of the top three trading partners of the Philippines. In 2022, the United States announced funding for the development of nickel and cobalt processing facilities in the Philippines with the support of USAID. The agency will also support the Advanced Manufacturing Workforce Development Coalition in the Philippines, which aims to leverage $5.3 million from the private sector to support advanced manufacturing.

10. Australia

Australia is a strategic ally of the United States. Historically, Australia has not been a key player in the semiconductor industry, relying on imports of its semiconductors, 87 per cent of which come from China.

A departmental study by the NSW government found Australia already has semiconductor design capabilities in radio frequency, millimeter wave, photonics and radar. It also has known deposits and reserves of several key semiconductor manufacturing materials, such as silicon dioxide and cobalt, as well as the research talent and equipment to design high-end chips.Australian domestic research institutes advise the government, as long as they give enough time and enough funds(Initial estimate requires $1.5 billion in initial investment and incentives)Australia can return part of the semiconductor design and manufacturing process to the mainland.

11. New Zealand

Center for Strategic and International Studies(CSIS)It is believed that IPEF is a supplement to the “reflow” of the industry promoted by the chip law, and its development goal is only “friendly shore outsourcing”, which is centered on the development of the US semiconductor industry, rather than promoting the development of the semiconductor industry itself in various countries. Therefore, under the U.S.-centered industrial system, CSIS recommends that the U.S. in the IPEF framework: establish reliable trading partner standards, establish mutually beneficial partnerships, expand information sharing, attract foreign talents and investment, promote trade facilitation, and ensure transparency in policy implementation.

The United States is revitalizing industrial policy through the Chips and Science Act and establishing a new regional trade architecture with partner countries through IPEF. The United States is working hard to strengthen its domestic and foreign semiconductor supply chains through cooperation with partner countries, and hopes to establish a more secure semiconductor supply chain within IPEF and deepen economic integration with these partners. The United States proposes the strategy of “friendly shore outsourcing”, whose essential goal is to de-Sinicize the global supply chain. “Friendly shore outsourcing” will be an important supplement to the industrial return policy promoted by the “Chip and Science Act”, and it is crucial to the US semiconductor strategy.

{kind=link}